With the SpaceX IPO now complete and registration filings for OpenAI and Anthropic in place, we have some idea of the forthcoming supply shock. Broadly, these transactions, along with the IPOs of Databricks and Anduril, represent upwards of $4.4 trillion of equity slated to come public. Weighed against the $67.5 trillion capitalization of the Russell 3000, this translates to an increase in supply of 6.6%. However, because the market price is set by the marginal buyer, the headline figure understates the impact, which will be far greater than Wall Street observers anticipate.

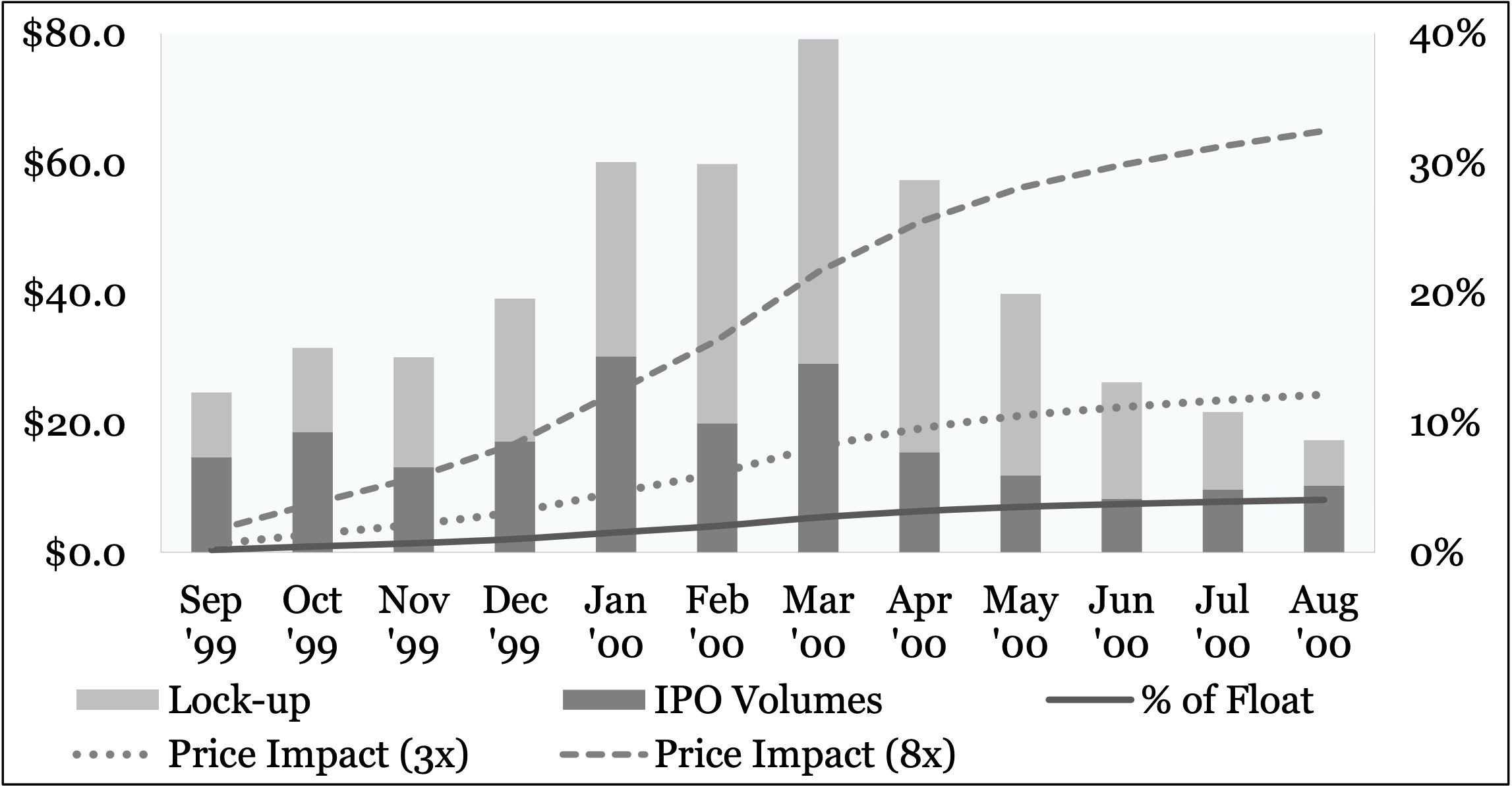

To understand the forthcoming supply impact, one needs only consider the experience during the Dotcom Bubble, which represents the closest comparable to the present. Per Figure 1, IPO volumes doubled from $14.7 billion in September 1999 to $29.2 billion in March, before being halved in the ensuing month. Sharper still, though, was the volume of newly-listed shares under expiring lock-up agreements – that prevented insiders from selling typically then for 180 days – which peaked at $50 billion in March 2000, when the floor supporting stock prices suddenly broke. As explained elsewhere, the influx of shares produced a crowding-out that, uniquely, explains the crash-like declines evidenced not only in 2000, but also in every other stock bubble for which data is available.[1]

Figure 1. Supply of New Stock vs. Percentage of Float, Price-Impact at 3x-8x

Source: Bloomberg, Ofek and Richardson (2003). Note the percentage of float based on cumulative supply, while the implied 3x–8x price impact is derived from Gabaix and Koijen (2021).

Of course, at 3.2% of the total float, the cumulative supply increase appeared modest in April 2000. Yet, the figure is deceptive. This is because demand for stocks is not perfectly elastic but dependent on the marginal buyer, whose absence is the very definition of a market panic. For this reason, Gabaix and Koijen (2021) estimate a price impact of three to eight times supply.[2] On that arithmetic, a 3.2% overhang indicates a decline between 9.6% and 25.5%. That the Nasdaq fell 37.3% in the 11 weeks after its peak in March 2000 suggests, unsurprisingly, that panic conditions command the high end of the range.

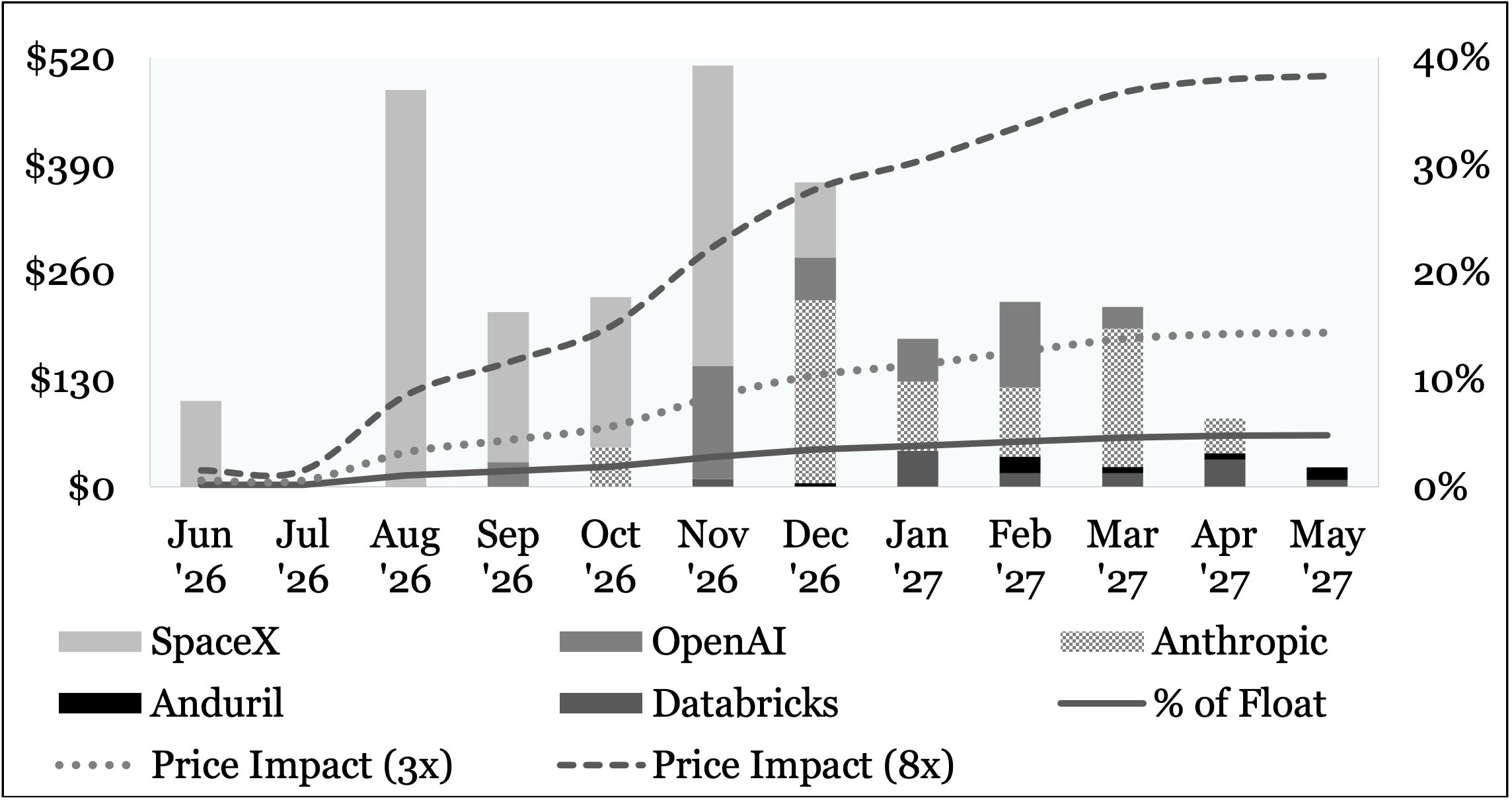

When the experience in 2000 is set against the present, it is evident that the governing determinant is not the headline issuance but rather the supply of unlocked shares. Because SpaceX has replaced the once-standard 180-day lock-up period with a multi-tiered scheme, the release of its public float will necessarily be different. To unpack further, the forward picture can be brought into focus if the novel lock-up schedule of SpaceX is applied to the private market valuations of the four mega-IPOs anticipated in the back half of 2026, including OpenAI, Anthropic, Databricks, and Anduril. Assuming OpenAI and Anthropic pursue IPOs in September and October, respectively, we can expect the volume of unlocked shares to reach 3.5% in December 2026, when the increase will outrank the experience in April 2000.

Figure 2. Illustrative New Supply vs. Percentage of Float, Price-Impact at 3x-8x

Source: Company registration statements; Bloomberg. Note the percentage of float based on cumulative supply, while the implied 3x–8x price impact is derived from Gabaix and Koijen (2021).

To be clear, all else equal, a supply increase of 6.6% is not necessarily cause for alarm in its own right. Instead, the danger lies in its combination with stretched valuations and elevated margin levels. Indeed, were these factors ill-present, the rotation elicited by the IPO volumes would lack the capacity to induce the same crash-like price declines. Yet, at the same time, the imbalance of supply over demand in an exhausted marketplace, where resources are spent, and margin accounts flexed, ensures the outcome. And while these preliminary figures are subject to great change, it stands to reason that the benchmarks achieved during March 2000 will be eclipsed in the immediate forecast period. For those in doubt, one need only consider how a well-placed step has the capacity to manifest an avalanche from a dormant snowpack. It is the nature of certain things.

Charles Lister Smith, PhD

June 26, 2026