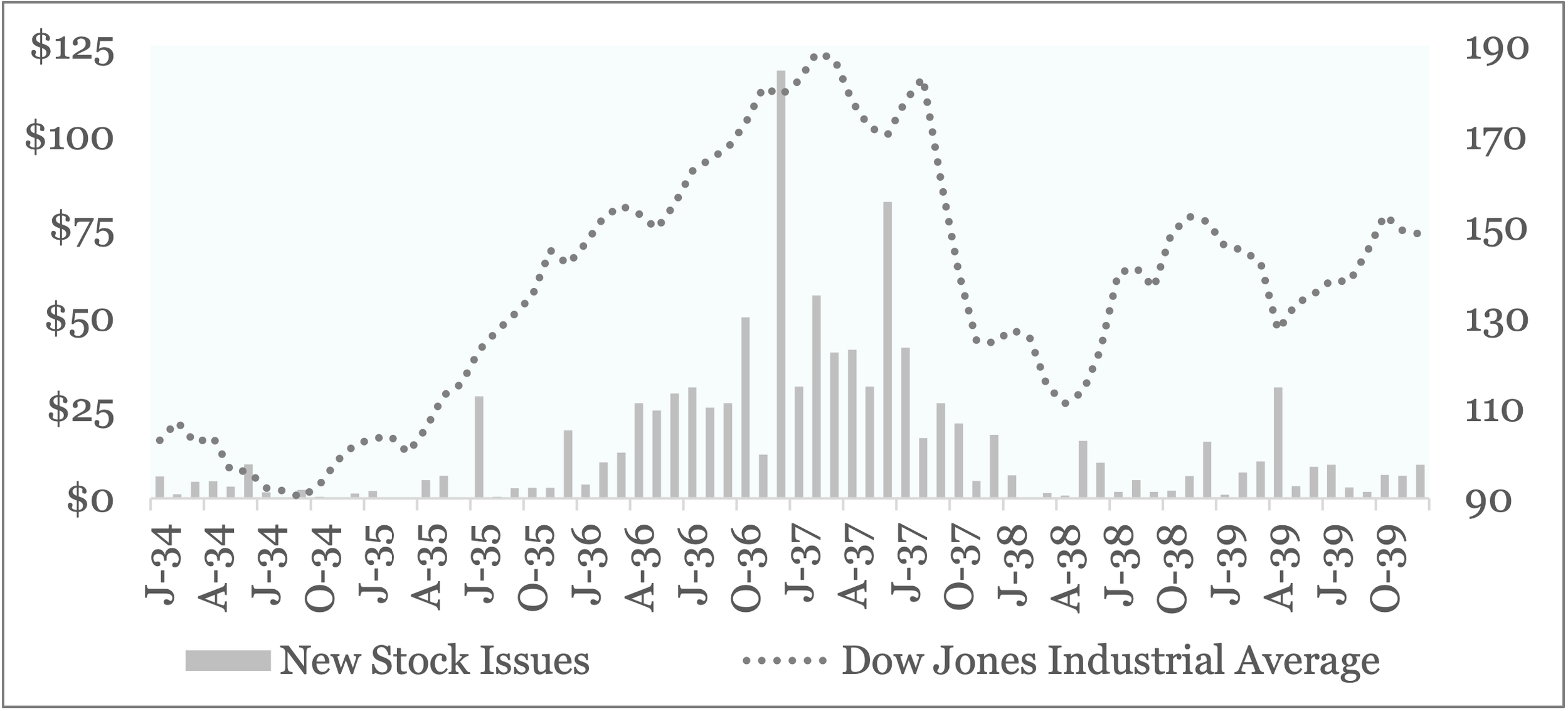

The Recession of 1937 was preceded by a material recovery in the U.S. capital markets that was spurred by an expansion in the money supply, which rose 23.4% (from $36.8 billion) to $45.5 billion in the two years from March 1935. Contributing further, the movement of foreign long-term capital was estimated at $462 million in 1935 and $758 million in 1936.[1] In concert, the DJIA gained 101 percent (from 96.71) to a cyclical high of 194.40 in March 1937. Having been “practically closed,” the new issues market underwent a “gradual revival” in the same period, when new stock issues leaped from $69 million in 1935 to $368 million in 1936.[2]

Figure 1. New Issues of Stocks vs. Dow Jones Industrial Average

Source: Monthly figures from the archives of the Federal Reserve Bank of St. Louis.

The upswing was notably shaped by the Revenue Act (1936), which contained an Undistributed Profit Tax provision that incentivized corporations to return cash to shareholders. Consequently, corporate dividends leaped from $2.8 billion in 1935 to $4.5 billion in 1936 and $4.7 billion in 1937. These elevated dividend payouts, importantly, combined with gold imports to cause an accelerated increase in bank reserves. And rather than allow a potentially ephemeral extension of credit, the Federal Reserve Board tightened reserve requirements on three occasions in the six months from August 1936.[3] While some argue the gesture restricted the amount of lending – and therefore contributed to the following contraction – it is better understood as preventing a sudden extension in credit.[4]

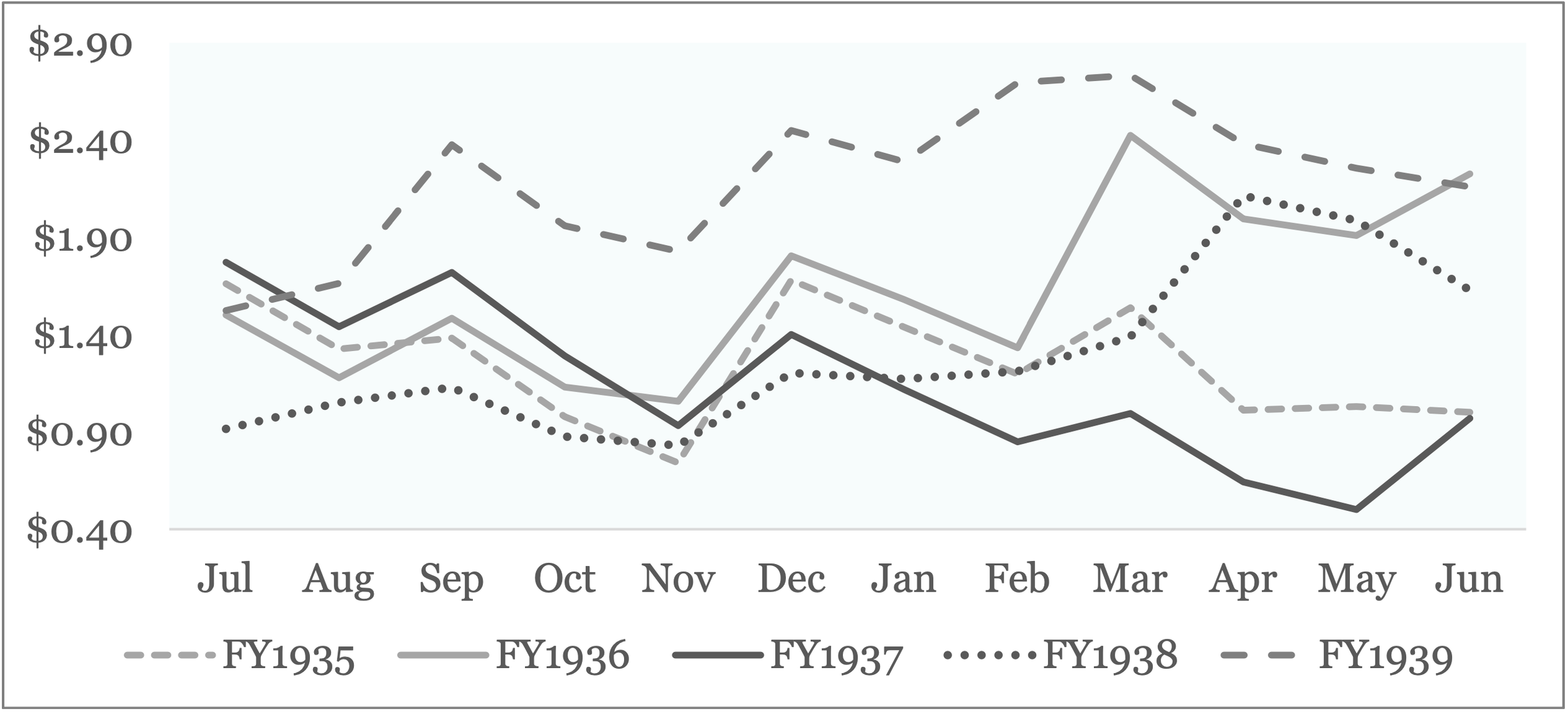

What is clear is that the market turned downward in March 1937, when the U.S. Treasury found itself with a budget shortfall that was driven by changes in the Revenue Act (1936). Rather than raise the funds in the new issues market, where the offering would have competed with the upturn in IPOs, the U.S. Treasury drew upon government deposits held in member banks of the Federal Reserve System. Per Figure 2, this decision reduced the latter to $0.9 billion in March 1937, when the balance reflected a $1.4 billion decline over the prior year. Seemingly innocuous and somewhat obscured by the seasonal swing, the action also caused a release of collateral that explains the sudden decline in U.S. Government securities held by member banks.[5] Further, while not obvious, the loss of government deposits also deprived banks of surplus funds – otherwise put at their discretion – that were routinely deployed in the new issues market.[6]

Figure 2. Working Balance of the U.S. Treasury, FY1935-39

Source: U.S. Treasury, Annual Reports (1935-39).

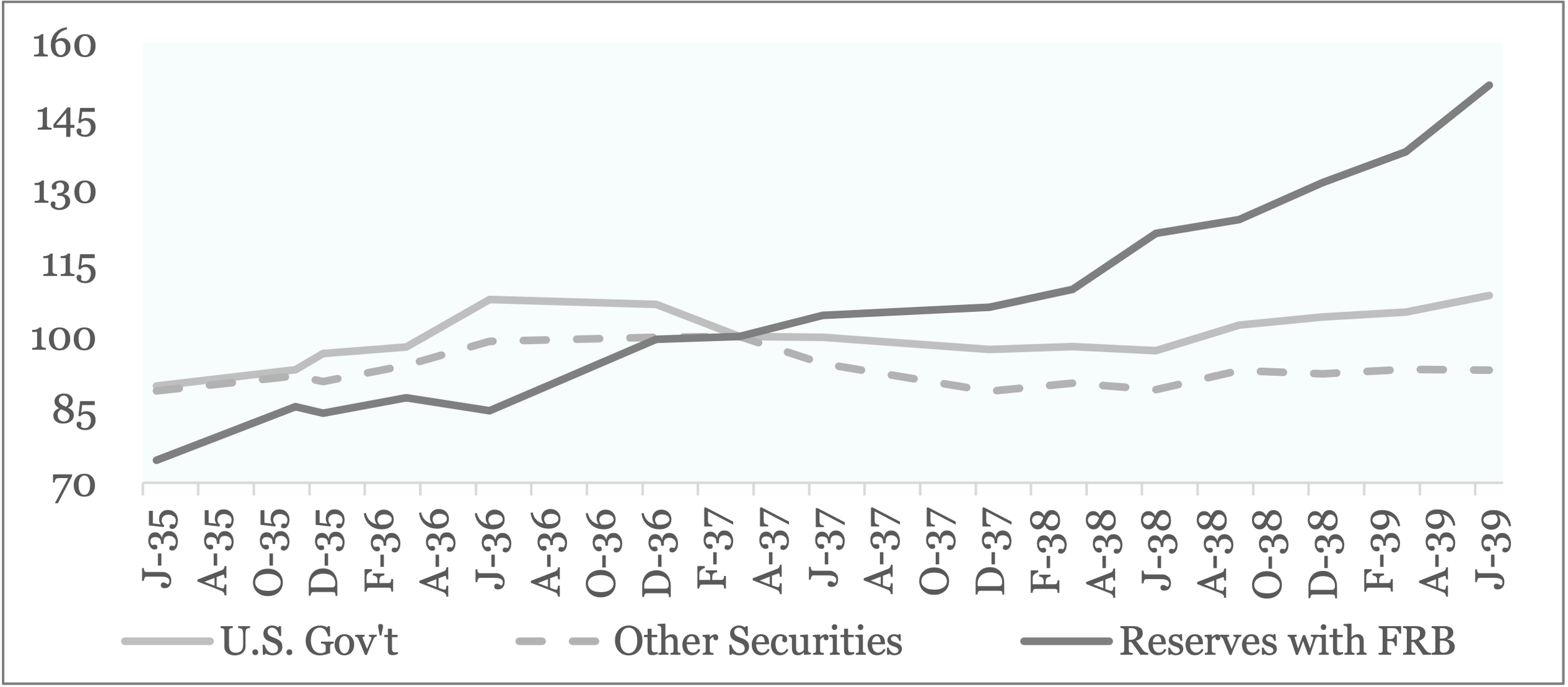

With the latter tendency adopted as procedure in May 1937, when Secretary Morgenthau announced the U.S. Treasury had abandoned its policy of maintaining a billion-dollar working balance, member banks were found without the same surplus funds and, therefore, burdened with unsold new issues.[7] Consequently, despite the continued growth in reserves, banks began to unwind positions, as reflected (see Figure 3) in a decline in Other Securities. Thereafter, the overhang of securities remained in place through December 1938, when FRBNY First Vice President Allan Sproul told Morgenthau that “the total of undigested securities on dealers’ shelves appears to be greater now than at any time since the autumn of 1937.”[8] Thus, while the U.S. Treasury did not openly compete with corporate offerings in the marketplace, its conduct indirectly contributed to a seizing-up in the new issues market, where banks were suddenly burdened with undigested securities that narrowed, if not closed, the IPO window altogether.

Figure 3. Reserves, U.S. Gov’t, & Other Securities held by Member Banks

Source: Federal Reserve Bank of St. Louis.

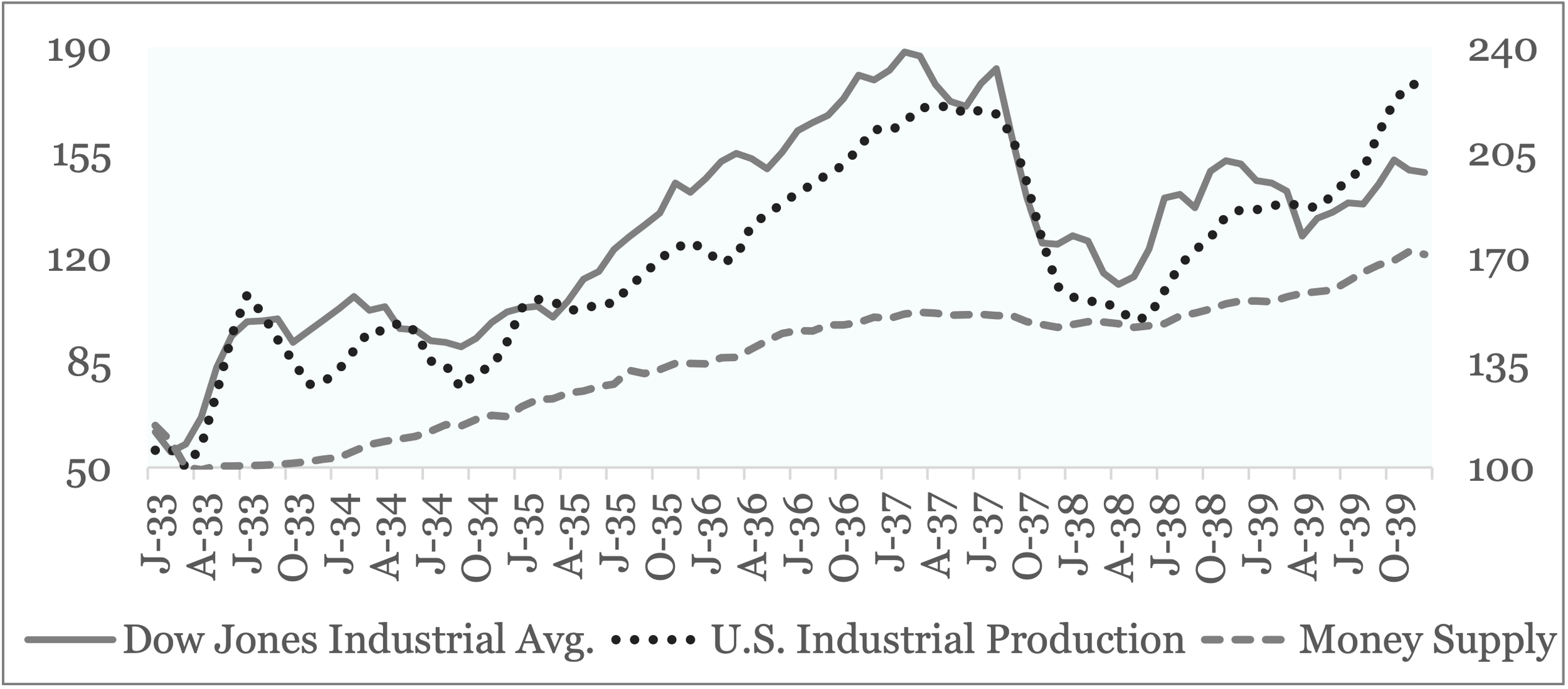

In the four months from March 1937, the congestion in the new issues market fed a gyration in market prices, as the DJIA slid 14.9% (to 165.51) before rising 14.8% (to 190.02) to within 2.3% of its prior peak. What followed then defied all expectations, as the support underlying market prices vanished altogether in conjunction with a sharp drop in production. Indeed, in the eight months ending March 1938, the DJIA plummeted 49.1% (to 98.95) alongside a 35.5% fall in industrial production. Occurring amidst a geopolitical shock, which consisted of no less than the outbreak of the Sino-Japanese and Spanish Civil Wars as well as a reversal in cross-border ‘hot money’ flows, the period was marked by a drop in public works spending that many have reasoned is the basis for the decline in industrial activity.[9] Additionally, scholars have pointed to the Soldiers Bonus in 1936 that provided impetus for manufacturers to overextend inventories.[10] However, these items, together, fail to explain the sudden stop in industrial production.[11]

Figure 4. DJIA vs. U.S. Money Supply and Industrial Production.

Source: Monthly data from FRED. Figures for U.S. Money Supply and Industrial Production are indexed to January 1933.

Instead, a not insignificant portion must be attributed to the U.S. Treasury’s decision to structurally lower the balances of government deposits that stripped the participating member banks of surplus funds deployed in the new issues market. Such a notion is supported by the stunning turnaround in industrial production during 1938 that, by all accounts, is attributed to the decision of the Roosevelt Administration to release the sterilized gold ‘profits’ held in the Treasury.[12] Described by one White House official as a “shot in the arm,” this action provided “reflation of a double-barreled sort” in April 1938, when the working capital of the balances of the Treasury was structurally lifted by $1.5 billion to $2.1 billion.[13] Complementing this action, the Roosevelt Administration championed a repeal of the Undistributed Profit Tax in May 1938 that restored the tax revenues that prompted the drawdown on deposits in the prior year. And, if the recovery hinged on an expansion in government deposits, it follows that the elimination of the same mechanism could only have created the initial deficit.

Where the drivers of decline are difficult to unpack, it stands to reason that the outsized decline in the DJIA was only achievable because of the oversupply of securities in the marketplace. Put simply, had the market not been inundated with supply, the legislative missteps brought about by the Revenue Act (1936) would not have resulted in a 49.1 percent decline in the DJIA in just eight months. Mirroring the experience in 1919, the episode in 1937 was marked by an overabundance of long-dated U.S. Government securities that was manifested by a surge in corporate issues. However, the events differed in that the repricing of U.S. Government securities evidenced in the former was checked in the latter by the sterilization of gold profits. And while unique in form, the descent of the DJIA is representative of the steep declines that can be anticipated in stock prices when the marketplace is suddenly confronted with an oversupply of risk-free securities.

Charles Lister Smith, PhD

July 14, 2026

[1] M.F. Jolliffe, “The Movement of Capital to and from the United States in 1935 and 1936,” Quarterly Journal of Economics, vol. 53, no. 1 (1938), 151.

[2] FRBNY, “Financing of Business Spending,” November 17, 1937, Box 45, Folder 6, Item 1, Marriner S. Eccles Papers, 10, https://fraser.stlouisfed.org/archival/1343/item/465394.

[3] Federal Reserve Board, Bulletin (May 1937), 1.

[4] This monetary action is blamed in the consensus opinion of Friedman & Schwartz (1963) for the ensuing downturn that commenced in March 1937. Yet, in the same quarter when member banks unwound $827 million of U.S. Government securities, bank reserves rose by $41 million alongside an increase in other securities of $13 million. These movements suggest the disturbance arose from other quarters, a notion that corroborates with the path of market yields, as shown in Figure A1.

[5] "Member Banks Reduce Government Holdings $196,000,000 in Week," Wall Street Journal, March 23, 1937, 8.

[6] Per David Kinley (1910), the accumulation of government deposits was responsible for a similar outgrowth in new security issues prior to the Rich Man’s Panic (1903) and Panic of 1907.

[7] "Treasury Silent on Financing Plans: Morgenthau Says Policy on Issuing of Bills Will Not Be Changed," New York Times, May 11, 1937, 37.

[8] Memo from Allan Sproul dated December 23, 1938, Diaries of Henry Morgenthau, Jr., vol. 157, 297. https://fraser.stlouisfed.org/archival/6880/item/634730.

[9] After recording net inflows of $813 million, the U.S. incurred foreign outflows of $575 million in the last three months of 1937, of which $130 million is attributable to Switzerland, $110 million to the U.K., and $80 million to the Netherlands (Federal Reserve Board, Bulletin (June 1938), 484-85).

[10] Kenneth D. Roose, “The Recession of 1937-38,” Journal of Political Economy, vol. 56, no. 3, 239-248, at 242; Alvin H. Hansen, Fiscal Policy and Business Cycles (W.W. Norton & Co., 1941), 64-65.

[11] In the 12-months ending June 1938, Public Works declined 20.1% to $880 million, a fall of just $222 million (U.S. Treasury, Annual Report for 1938, 5).

[12] Douglas A. Irwin, “Gold Sterilization and the Recession of 1937-38,” NBER Working Paper Series, Working Paper 17595 (November 2011).

[13] Bernard Kilgore, “Some U.S. Officials Ponder Plan To Use ‘Profits’ From Gold,” Wall Street Journal, December 7, 1937: 1; Morgenthau attributes the bold decision to President Roosevelt, whom he describes as being “really scared to death” in April 1938 (Henry Morgenthau, Jr., “Presidential Diaries,” book 1 (April 11, 1938), 2, https://fraser.stlouisfed.org/archival/6880/item/635449). While no record exists, it is not unreasonable to assume the reflation scheme was modeled after the experience in March 1933, when the same mechanism was produced with an injection of notes in circulation. Visible in Figure A-2, the relationship sits outside existing scholarship that attributes the reflation (only) to a change in business confidence.